Renegotiating your mortgage at renewal time is an excellent way to save money and ensure that you have the best mortgage product for your financial situation. “51% of Canadian homeowners don’t plan on changing lenders when their mortgage comes up for renewal — and 9% weren’t even aware that they could switch lenders to get a better rate.” says Shaistha Khan by Rates.ca. Here are five reasons why you should explore your options for mortgage renewal instead of staying with the same lender’s offer:

Get a Better Interest Rate

One of the most significant benefits of exploring your options for mortgage renewal is the chance to get a better interest rate. Interest rates can fluctuate significantly over the term of a mortgage, and you may be able to find a better rate at the time of renewal. Even a small decrease in your interest rate can save you thousands of dollars over the life of your mortgage.

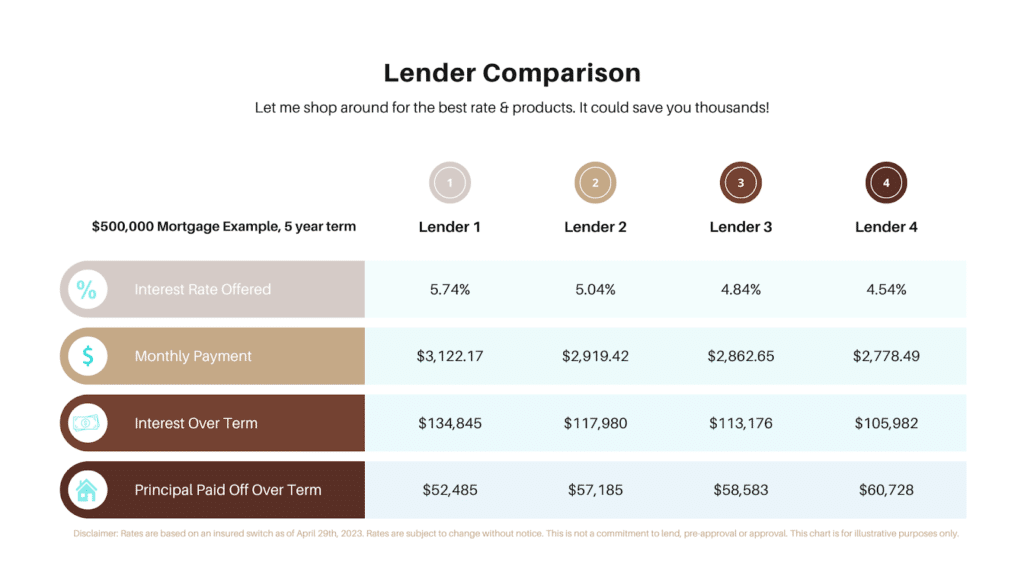

The above illustrates the difference approximate interest rates currently offered by 4 lenders in todays market. When comparing Lender 1 and Lender 4, there is a financial difference of $343.68 per month ($20,620.80 over your 5 year term), not to mention that you will end up paying approximately $28,863 more in interest with Lender 1 over your term.

Save Money on Fees

In addition to interest rates, mortgage products can vary in terms of fees and penalties. By exploring your options for mortgage renewal, you may be able to find a mortgage product with lower fees or more favourable penalties. This can save you money if you need to break your mortgage early or make changes to your mortgage terms. Also, the majority of lenders will cover the costs for you to switch your mortgage to their institution.

Improve Your Financial Situation

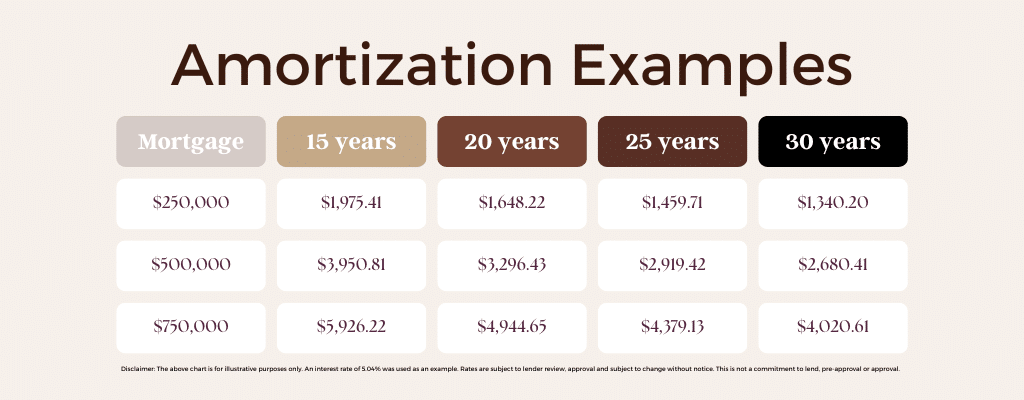

Your financial situation can change significantly over the term of your mortgage. If you’ve experienced a change in income, lifestyle, or financial goals, exploring your options for mortgage renewal can help you find a product that better suits your current needs. For example, you may be able to switch from a fixed-rate to a variable-rate mortgage if your income has increased, or you may want to switch to a shorter term if you’re planning to retire soon. Another option for those struggling with cashflow is to extend their amortization out to 30 years.

Access Equity in Your Home

If you’ve built up equity in your home over the term of your mortgage, exploring your options for renewal can help you access that equity. You may be able to refinance your mortgage and take out a larger loan, using the extra funds to pay off debt, make renovations, or invest in other assets. This can be a great way to leverage your home’s value and improve your overall financial situation.

Don’t be fooled by low interest rates

The lowest mortgage rate doesn’t always mean the best deal. Here are some things to consider when researching, lenders, mortgage terms & interest rates.

- Not all mortgages are the same, even if they have similar rates

- Beware of “Restricted Mortgage Products” that may have hidden terms and conditions

- Read the fine print to ensure you’re not committing to a bonafide sales clause (the need to sell your home in order to break the contract/term) or other unfavorable terms

- Look for flexible mortgage options with reasonable prepayment privileges and penalty calculations

- Don’t be lured by rates that seem too good to be true – they probably are

In conclusion, exploring your options for mortgage renewal is a smart financial move that can help you save money, access equity, and improve your overall financial situation. By taking the time to research different mortgage products and negotiate with lenders, you can find a product that meets your current needs and provides the best value over the long term. Before you sign on the dotted line, make sure you do your research and understand all the terms and conditions of your mortgage agreement. Your financial future may depend on it.

{kind=link}

{kind=link}